Are We Ready for Regulations Yet?

Are We Ready for Regulations Yet?

Some businesses are, but they only whisper about it

On April 16, Ezra Klein started a New York Times opinion piece thusly:

Among the many unique experiences of reporting on A.I. is this: In a young industry flooded with hype and money, person after person tells me that they are desperate to be regulated, even if it slows them down. In fact, especially if it slows them down.

What they tell me is obvious to anyone watching. Competition is forcing them to go too fast and cut too many corners. This technology is too important to be left to a race between Microsoft, Google, Meta and a few other firms. But no one company can slow down to a safe pace without risking irrelevancy. That’s where the government comes in — or so they hope.

This may be a unique recognition in modern journalism - certainly at the New York Times - but it’s not the first time I have heard of industry saying, even on the sly, “Competition is leading us to do bad things; we need to be regulated.”

Hell, this isn’t even the first time in the last month that the Times - and other mainstream news outlets - have reported on business catastrophes that were caused by not enough regulation.

In his 2013 book, “Salt, Sugar, Fat: How the Food Giants Hooked Us,” Michael Moss writes about the idea of a “bliss point” in snack food manufacturing, and a failed attempt in 1999 by a senior executive of Kraft Foods to get the industry to regulate itself. This executive, Michael Mudd, wanted to redefine that bliss point - and snack food marketing - to take health considerations into effect.

His attempt failed miserably. Or, perhaps we can say, crumbled into salty dust. Mudd’s fellow food company executives didn’t see children, or even their parents, as their primary concern. Moss quoted the CEO of General Mills: “We need to ensure that our products taste good because our accountability is also to our shareholders.”

I guess shareholders don’t get high cholesterol.

Ron Suskind, in his 2011 book, “Confidence Men,” wrote about a meeting he attended of financial industry folks, who told him, essentially, that before the 2008 financial crisis, they played the game that was given to them, and they pushed the boundaries because there were no rules to stop them. More to the point, they said they would do it again unless the government wrote rules.

Of course, the financial industry howled at the Dodd-Frank Wall Street Reform and Consumer Protection Act, which only partially restored the banking regulations of Glass-Steagall, which were gutted by the Clinton Administration in the 1990s, which led first to the Enron bankruptcy and then to the 2008 crisis.

But the financial industry is about profit above all else. So their lobbyists - who are paid by what they get through Congress, not for the health of the financial system - pushed through a softening of Dodd-Frank in 2018.

This new law, which was vehemently opposed by Senator Elizabeth Warren, raised the threshold of stricter regulation from banks with $50 billion or more in assets to banks with $250 billion or more in assets. This means most of the banks in the country that, since Dodd-Frank was passed, had to subject themselves to stress tests and stricter oversight by the Fed, suddenly were off the hook.

One of those banks was Silicon Valley Bank.

We all know that SVB no longer exists, and its sudden collapse almost triggered a system-wide banking meltdown. And we know that its former CEO, Greg Becker, was one of the banking leaders pushing for the 2018 reform.

This week, we are seeing the FDIC take over another niche bank - First Republic, which mostly created mortgages for the super-rich at rock-bottom interest rates. Like a $5.95 million mortgage for Mark Zuckerberg at 1.05%.

I’m not exactly sure which number shocks me more. Or why I’m shocked at all that the more money people have, the less money we ask them to pay.

But discounting interest rates is a risky business when the chief oversight entity - the U.S. Fed - is raising interest rates. So is putting most of your eggs in one basket.

Thus, government has to intervene to help sell off the bank - and its highly desirable customers - to one of the “too big to fail” banks with assets over $250 billion. By the way, First Republic’s assets are $233 billion. Just under the regulatory threshold.

We also learned this week that the Fed had the ability to oversee both SVB and First Republic, but didn’t bother - and now they’re kicking themselves for it.

What’s missing in the Fed’s self-flagellation is any awareness that raising interest rates in the first place was the fuse that lit the fire. Never mind that there is a pretty large hew and cry from economists and economics writers like Robert Reich, and Claudia Sahm, and Zach Silk, and Joseph Politano that higher prices are caused by corporate price gouging and not too much employment; and that these interest rate hikes are essentially based on a misdiagnosis. What’s clear to me is that even if raising interest rates was a good idea, the Fed clearly had no clue that there were financial institutions that would suffer.

Let’s go back to this lit fuse metaphor. If you attach dynamite to a long detonating fuse, and toss it over a hill, you really should make sure there’s not someone or something on the other side of the hill before you light it.

The Fed has the ability to both hike interest rates and oversee banks. If it had coordinated both of these tasks - whichever way they decided - we wouldn’t be freaking out over the health of our banking systems and economy.

Rules of the Road

Decades of child-rearing research has shown that children do better with clearly articulated rules and expectations. We all do, actually.

We have lanes on roads, and stop signs and traffic lights to avoid the chaos that might emerge if drivers just decided to do their own thing. We just passed Tax Day, and the vast majority of people in this country filed their taxes.

Hell, the rules don’t even have to be government mandated. I’ve been flying a lot this past year, and wracking up the points on Southwest. It amazes me, every time I get in line to board, the people around me check with one another about what our number is. And we willingly and happily change places with someone who has a lower number than ours. Because it’s a fair rule. And rather than creating stress, it actually encourages camaraderie. “You’re number 32, what are you doing all the way back here! Get up to the front!”

It’s not rules that are bad, it’s the thinking behind them - or lack thereof - that gets us in trouble. The AI industry is begging for regulation. The Fed is pissed at itself for not regulating enough. And social media users are constantly talking about content moderation. Yet, we still have journalists and lawmakers who have never found themselves questioning the dictum that “regulations are bad.”

It’s strange to me. When children throw public tantrums because they can’t self-regulate, the world passes judgment on their parents’ abilities to control their children. When bankers fail to self-regulate, we shrug.

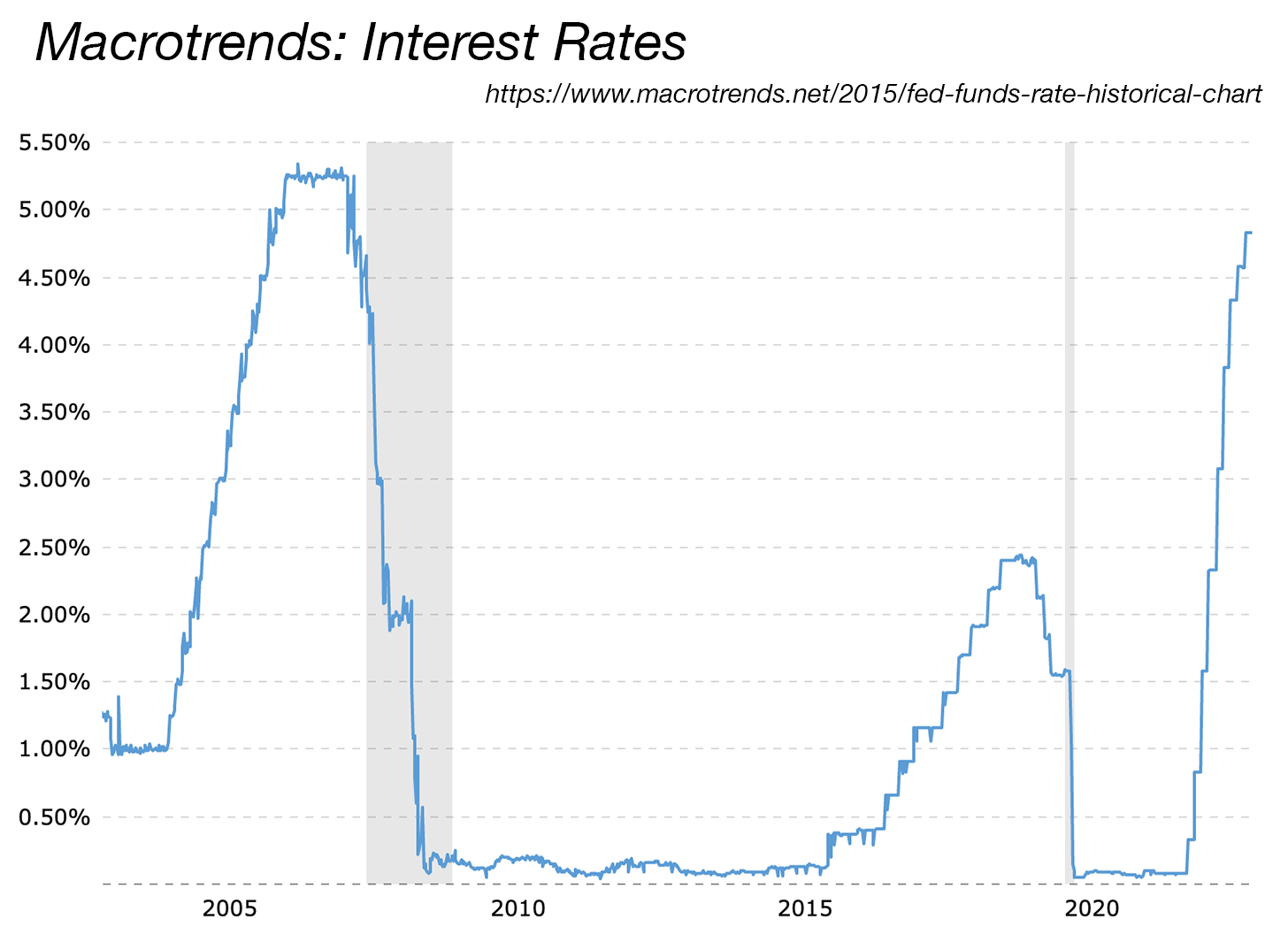

A Bit More On Interest Rates

This graph is fascinating to me. It’s interest rates from 2004 to today. What I’m seeing is that the Fed - sensing an overheating economy - started raising interest rates in 2005, but that didn’t head off the biggest economic downturn since the Great Depression. Because the underlying issue was deregulation that led to financial instruments like mortgage-backed securities (taking bits and pieces from different mortgages and creating a totally different entity) and financial institutions that were too interconnected. Like the old Christmas tree bulbs, that would take the whole string out if one bulb shorted.

The interest rate hike now looks similar to the one in 2005, and I fear that there are other underlying issues that the Fed doesn’t have the ability to cure.

But Congress does. The issues with our financial system - which had been stable for five decades after the implementation of the New Deal - were caused by government policy change, specifically around guardrails and regulation. We still need government to step up and regulate. The difference between now and the 1980s and ‘90s, though, is that we have people in Congress who want to regulate, who are staking their entire careers on reigning in Voodoo Economics.

But how many of my fellow journalists will write or broadcast about those ideas?